3 Things 8-11-25

- Oct 22, 2025

- 5 min read

Thing One

How Much Should You Have Invested In Stocks?

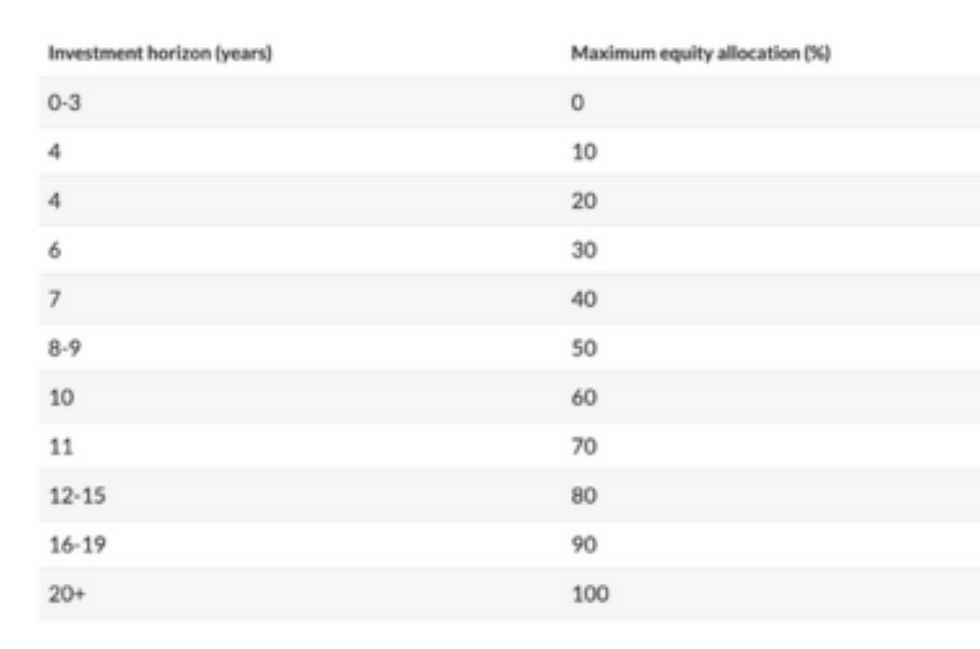

While there are many financial practitioners who will answer this precisely after you provide them with a few pieces of information, there really is no one “right” answer to this question. That said, there are some very useful guides that you can use to help you decide on an appropriate number for your situation. For example, the chart below suggests that if your investment horizon, the period of time from now until you actually need to use the money, is zero to three years, you should not have anything in stocks while if you have more than a twenty-year investment horizon, you should have all of your available investment dollars in stocks.

Now, before you run with this, remember there are no absolute formulas and there are potentially lots of things that can make person A’s number different from person B’s. Chief among them would be how the term, "investment horizon", is defined in detail. In other words, what does the end of the horizon represent, death or retirement or something else? Do they need to use all the money at once at the end of the horizon? If they don’t need to use all the money, how much risk are they willing to take with the “spare cash”? The questions can go on and on, but you get the point. It’s a useful guide but not a one-size-fits-all solution. As always, you should know we can help you or people you know and care about work through what makes the most sense in your specific situation. Just reach out or let them know to do the same.

|

|

Thing Two

From the archives of the blog that was the inspiration for this newsletter...

Some (Useful) Bias Training

"It’s funny what a bull market can do to our brains. . . .

Money earned passively in the market, rather than from toiling at work, can feel easier to gamble with. It is a dangerous bias psychologists call the “house-money effect.”. . .

Everyone wants to assume that they can think rationally. But with bear markets now a fading memory . . . now is an important time to understand the common behavioral biases that cause investors to make regrettable decisions during bull markets.

Here are five others.

The backfire effect. This is a powerful bias that causes us to double down on our beliefs when exposed to opposing viewpoints.

“We think this response occurs because people respond defensively to being told that their side is wrong about a controversial factual issue,” says Brendan Nyhan, an assistant professor of government at Dartmouth College, who has studied the backfire effect in politics.

“In the process of defending that view, they can end up convincing themselves to believe it even more than they otherwise would have if they had not been challenged,” he says.

The same flaw can run wild in investing debates.

If you are convinced that we are in a lasting bull market, how do you feel when you hear someone say that stock valuations are historically high, or that we are overdue for a correction?

If you find yourself so critical of opposing views that you become even more convinced the bull market will last, watch out. Once your priorities shift from determining the truth to blindly defending your original views, you have lost the ability to think rationally.

Confirmation bias. This flaw causes us to seek out only information that confirms what we already believe.

Access to financial opinions has exploded in recent years . . . . But it can be dangerous, because no matter what you believe—and no matter how wrong those beliefs may be—you can likely find dozens of investors who agree with you. Having other people confirm your views may cause you to become more convinced that those views are correct.

Charles Darwin had a knack for obsessing over information that disproved his own theories. Investors should try to do the same.

Anchoring bias. This phenomenon causes us to cling to an irrelevant piece of information when estimating how much something is worth.

Your opinion on how much a stock is worth may be anchored to how much you paid for it. If you paid $100 for a share of Apple stock, you are probably more likely to think shares are worth more than $100 than another investor who paid $80 for the stock.

But the market doesn’t know how much either you of you paid for the shares. And it doesn’t care what either of you think is a fair price. Markets will do as they please, regardless of what price you are fixated on.

Recency bias. This one is simple: It is another term for the tendency to use the recent past as a guide to the future.

People like patterns. If stocks have just gone up, the natural tendency is to assume they will keeping going up—at least until they go down, and then we assume they will keep going down....

Markets move in cycles, but people forecast in straight lines. That is recency bias, and it is particularly dangerous after a long bull market.

Blind-spot bias. This—the most dangerous investing bias—is a flaw that causes us to think the biases described above affect other people, but not ourselves."

Summing Up

Individual investing has to be a long term commitment in order to be successful.

Part of successful individual investing includes the ability to understand the role that our emotions and biases tend to play when stock prices decline.

Since we humans tend to react more quickly to negative events than to positive occurrences, we are much more likely to do the exact wrong things at market bottoms and tops. We too often panic and sell when the market is falling rapidly, and then turn right around and buy when stocks are rising.

That's the losing buy high and sell low 'model,' and it's harmful to one's long term financial health and well being.

So becoming better acquainted with our emotional side is perhaps the best thing we need to know about individual investing.

And the second best thing to learn is the power of compounding and the rule of 72 (money doubles each time the number of years multiplied by the percentage annual rate of return equals 72, as in 12 x 6, 9 x 8).

So start early, stay the course, and reap the long term benefits of a rising stock market. |

Thing Three

Just A Thought

"Without education, we are in a horrible and deadly danger of taking educated people seriously." - G. K. Chesterton |

Comments